“It’s a sad dog that won’t wag its own tail.”

—Southern Aphorism

In this spirit, I must share an anecdote that provides very strong support for my long-standing admonition to learn how to write software and program yourself out of a job, rather than wait until someone else does it for you, because if it can be automated, then it will be automated.

I began developing the practice utilities at Pecuniology.com in response to students’ requests for practice tests in the Managerial Finance courses that I teach. Previously, I distributed paper copies of sample numerical questions from old exams, and every time typos snuck in when I was not looking. No matter how careful I thought I was, I inevitably grabbed a version that had errors in it that were different from the version that I had distributed in the immediately preceding semester, and the cycle of duelling typos never resolved.

Over the years, the typos reproduced and mutated in a manner that had me afraid that I might wake one morning to find that they had evolved into something particularly virulent and maybe even achieve self-awareness.

Finally, a couple years ago, after having told nearly two thousand students over the better part of a decade that they should learn how to write software and program themselves out of jobs, rather than wait until someone else to did it for them, I decided to program myself out of a job. I’m not there yet, but I learned recently that I am closer than I had suspected, and that doing so has improved my teaching performance dramatically.

In a fit of frustration and in a mood to show off a bit, I followed my own advice to solve whatever problem annoys you the most, and converted those contemptible paper printouts into the first version of the online practice utilities linked to above.

During the first semester, students and I identified errors and omissions that, once corrected stayed corrected, and the flood of emailed pleas for help just prior to exams fell from a firehose to a trickle. This is in large measure, I since have learned, because I took the time to incorporate randomly generated values into the problems. In essence, anyone, anywhere in the world can create seemingly infinite variations on the questions posted, just by clicking the Reload button.

In response to the few cries for help that I do receive, I tend to post my replies in this Blog area, and respond more often than not with the URL of the post that addresses the question, along with exhortations to practice, practice, PRACTICE. When a student asks for further clarification, I edit my follow-up response into the existing post.

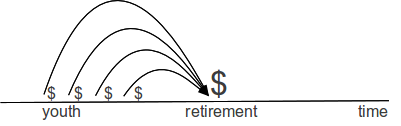

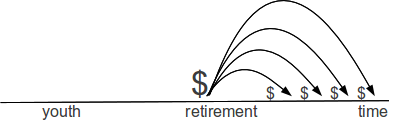

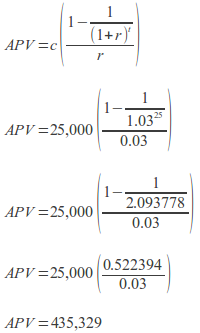

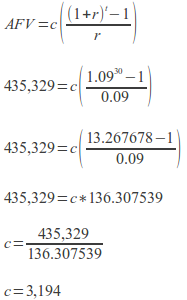

Shortly after I integrated those sets into my classes, I noticed a dramatic improvement in my students’ test scores and subsequently cranked up the pressure by asking more realistic (read ‘harder’) questions. For the Advanced Managerial Finance class, which we hold in computer labs, I have my students build spreadsheets that replicate each of the practice utilities and use those to answer some sample questions.

The first time that I was asked to teach Principles of Managerial Finance—one of the handful of dreaded required courses that all students in the College of Business must pass—online, I cringed at the thought of my students suffering in solitude, armed with only a textbook and the accompanying publisher-produced practice questions that are more about solving dense and clever puzzles than about preparing for a career of drafting business plans, seeking investment, and managing working capital accounts.

I envisioned each of them cowering in the dark by the light of a kerosene lantern, in a dank and fetid shack with the wind howling, panthers screaming into the night, and alligators banging their massive tails on the kitchen door—we’re in South Florida; that kind of thing can happen from time to time—as they tried to make sense of some of concepts that run exactly counter to virtually everything that their high school teachers and most politicians have told them most of their lives, like the promise of a benefit in the future is worth less than an actual benefit now, you will not necessarily be rewarded for bearing risk, there is a cost for every benefit, and the future is unknowable although it is not unimaginable. That, and we say it with algebra.

Thus were born the videos on the page that links to the utilities above. As I type this, that page is still as ugly as someone else’s baby pictures, and in one of them I had a cold when I recorded the voiceover. And, you know what? The kids love it.

I know this, because I just received my student survey results from the online section that just ended a couple days ago, and my scores are a thing to be envied. This is not because of any special treats that I hand out, as—and I hesitate to post this—I was horribly distracted this semester, and I had thought that I was largely AWOL. I half-expected them to burn me in effigy and call for my public humiliation. (I exaggerate, but only for effect.)

Granted, I make it a point to respond to email within 24-48 hours, but sometimes a four-day weekend turns into a one-week turnaround time (yes, inexcusable!). However, when I was remiss, students turned in their frustration to each other for help, and the vast majority of the time, a classmate directed the questioner to one of my videos or blog posts.

I am fast becoming the Andy Warhol of Business education, whose art is streamlining the creative process to the point where my own hand never touches the end product. And, with Direct Deposit, I don’t even have to endorse and cash the checks. (Again, I exaggerate, but not all that much.)

Here’s the kicker: I use the same exams, albeit with different numbers, in the classroom and online, and my mean scores and distributions are insignificantly different from each other! I very nearly have achieved the Holy Grail of ensuring that my online and face-to-face sections are as closely aligned as is possible.

So, to repeat, if you teach Business, especially Accounting, Economics, or Finance, learn how to write software and program yourself out of a job. Alternatively, contact me and have me do it for you. Seriously.

Invest accordingly.

Prof. Evans